Nature and purpose of management consulting

1.4The consulting process

An overview

During a typical consulting intervention, the consultant and the client undertake a set of activities required for achieving the desired purposes and changes. These activities are normally known as “the consulting process”. This process has a clear beginning (the relationship is established and work starts) and end (the consultant departs). Between these two points the process can be subdivided into several phases, which helps both the consultant and the client to be systematic and methodical, proceeding from phase to phase, and from operation to operation.

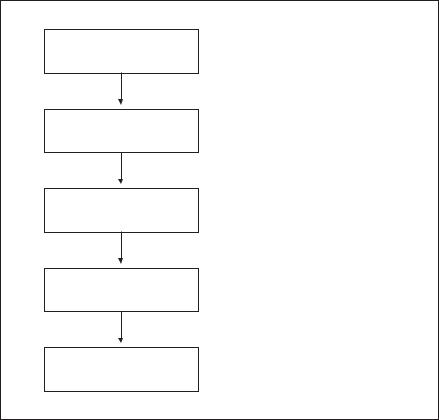

Many different ways of subdividing the consulting process, or cycle, into major phases can be found in the literature. Various authors suggest models ranging from three to ten phases.11 We have chosen a simple five-phase model, comprising entry, diagnosis, action planning, implementation and termination. This model, shown in figure 1.2, will be used consistently in our book. Obviously,

Figure 1.2 Phases of the consulting process

• First contacts with clients

• Preliminary problem diagnosis 1. Entry • Assignment planning

• Assignment proposals to client

• Consulting contract

• Purpose analysis

• Problem analysis 2. Diagnosis • Fact finding

• Fact analysis and synthesis

• Feedback to client

• Developing solutions

3. Action planning • Evaluating alternatives

• Proposals to client

• Planning for implementation

• Assisting with implementation 4. Implementation • Adjusting proposals

• Training

• Evaluation

• Final report

5. Termination • Settling commitments

• Plans for follow-up

• Withdrawal

21

Management consulting

a universal model cannot be applied blindly to all situations, but it provides a good framework for explaining what consultants actually do and for structuring and planning particular assignments and projects.

When applying the model to a concrete situation it is possible to omit one or more phases or let some phases overlap, e.g. implementation may start before action planning is completed, or a detailed diagnosis may not be necessary or can be integrated with the development of proposals. It may be useful to work backwards from a later to an earlier stage. Thus evaluation can serve not only for a final assessment of the results of the assignment and of benefits drawn from change (termination phase) but also for deciding whether to move back and take a different approach.

Every phase can be broken down into several subphases or parallel activities. The whole model has to be applied flexibly and with a great deal of imagination. The consulting process can be viewed as a variant of the change process (Chapter 4), one in which change is planned, managed and implemented with a consultant’s help. The reader may have seen various models of planned organizational change and may be interested in comparing them with the model in figure 1.2.

The consulting process will be examined in detail in Chapters 7–11, but at this point it will be helpful to have short descriptions of its five basic phases.

Entry

In the entry phase the consultant starts working with a client. This phase includes their first contacts, discussions on what the client would like to achieve or change in his or her organization and how the consultant might help, the clarification of their respective roles, the preparation of an assignment plan based on preliminary problem analysis, and the negotiation and agreement of a consulting contract.

This is a preparatory and planning phase. It is often emphasized that this phase lays the foundations for everything that will follow, since the subsequent phases will be strongly influenced by the quality of conceptual work done, and by the kind of relationship that the consultant establishes with the client at the very beginning.

In this initial phase, it can also happen that an assignment proposal is not prepared to the client’s satisfaction and no contract is agreed, or that several consultants are contacted and invited to present proposals but only one of them is selected for the assignment.

Diagnosis

The second phase is an in-depth diagnosis of the problem to be solved. During this phase the consultant and the client cooperate in identifying the sort of change required, defining in detail the purposes to be achieved by the assignment, and assessing the client’s performance, resources, needs and perspectives. Is the fundamental change problem technological, organizational, informational, psychological or other? If it has all these dimensions, which is the crucial one?

22

Nature and purpose of management consulting

What attitudes to change prevail in the organization? Is the need for change appreciated, or will it be necessary to persuade people that they will have to change? The results of the diagnostic phase are synthesized and conclusions drawn on how to orient work on action proposals so that the real problems are resolved and the desired purposes achieved. Some possible solutions may start emerging during this phase.

Fact-finding and fact diagnosis often receive the least attention. Yet decisions on what data to look for, what data to omit, what aspects of the problem to examine in depth and what facts to skip predetermine the relevance and quality of the solutions that will be proposed. Also, by collecting data and talking to people the consultant is already influencing the client system, and people may already start changing as a result of the consultant’s presence in the organization. Conversely, fact-finding has to be kept within reasonable limits, determined by the nature and purpose of the consultancy.

Action planning

The third phase aims at finding the solution to the problem. It includes work on one or several alternative solutions, the evaluation of alternatives, the elaboration of a plan for implementing changes and the presentation of proposals to the client for decision. The consultant can choose from a wide range of techniques, in particular if the client actively participates in this phase. Action planning requires imagination and creativity, as well as a rigorous and systematic approach in identifying and exploring feasible alternatives, eliminating proposals that could lead to trivial and unnecessary changes, and deciding what solution will be adopted. A significant dimension of action planning is developing strategy and tactics for implementing changes, in particular for dealing with the human problems that can be anticipated, and for overcoming resistance to, and gaining support for, change.

Implementation

Implementation, the fourth phase of the consulting process, provides an acid test for the relevance and feasibility of the proposals developed by the consultant in collaboration with the client. The changes proposed start turning into reality. Things begin happening, either as planned or differently. Unforeseen new problems and obstacles may arise and false assumptions or planning errors may be uncovered. Resistance to change may be quite different from what was assumed at the diagnostic and planning stages. The original design and action plan may need to be corrected. As it is not possible to foresee exactly and in detail every relationship, event or attitude, and the reality of implementation often differs from the plan, monitoring and managing implementation are very important. This is also why professional consultants prefer to be associated with the implementation of changes that they have helped to identify and plan.

This is an issue over which there has been much misunderstanding. Many consulting assignments end when a report with action proposals is transmitted,

23

Management consulting

i.e. before implementation starts. Probably not more than 30 to 50 per cent of consulting assignments include implementation. If the client is fully capable of handling any phase of the change process alone, and is keen to do it, there is no reason why he or she should continue to use a consultant. The consultant may leave as early as after the diagnostic phase.

Unfortunately, the decision to terminate an assignment after the diagnostic or action-planning phase often does not reflect the client’s assessment of his or her own capabilities and determination to implement the proposals without any further help from the consultant. Rather it mirrors a widespread conception – or misconception – of consulting according to which consultants do not have to achieve more than getting their reports and proposals accepted by the clients. Some clients choose it because they do not really understand that even an excellent report cannot provide a guarantee that a new scheme will actually work and the promised results will be attained. Other clients may be happy because what they really wanted was a report, not change.

Termination

The fifth and final phase in the consulting process includes several activities. The consultant’s performance during the assignment, the approach taken, the changes made and the results achieved have to be evaluated by both the client and the consulting firm. Final reports are presented and discussed. Mutual commitments are settled. If there is an interest in pursuing the collaborative relationship, an agreement on follow-up and future contacts may be negotiated. Once these activities are completed, the consulting assignment or project is terminated by mutual agreement and the consultant withdraws from the client organization.

A consulting assignment

In practice, the five stages of the consulting process are usually structured, organized and implemented through particular and separate consulting assignments (also called engagements, cases, consultancies, projects or client accounts). In a typical assignment, the consultant and the client agree on the scope of the job to be done:

–the purposes (objectives, results) to be achieved;

–the expertise to be provided by the consultant;

–the nature and sequence of tasks to be undertaken by the consultant;

–the client’s participation in the assignment;

–the resources required;

–the timetable;

–the price to be paid;

–other conditions as appropriate.

24

Nature and purpose of management consulting

This agreement is confirmed in a consulting contract, which is written in most cases, but can be verbal (section 7.6). The contract will determine the phases of the consulting process that will be covered by the assignment, e.g. the assignment will be completed when an analytical report has been submitted to the client.

Alternatives to separate consulting assignments

An alternative to an assignment covering a distinct task or set of tasks and period of time is a retainer. Under a retainer contract, the client purchases in advance a certain amount of the consultant’s time. The nature and purpose of the work to be done are defined in general terms only and will be specified at the beginning of each period covered by the contract. Collaboration extends over a longer period of time, using a cost-effective format. For example, the client may use the consultant’s services for two days during the first week of every month to review jointly the general situation of the business, the problems and opportunities that have developed and the key decisions that will have to be taken. Or the agreement may define a more or less regular task for the consultant (e.g. assisting management in preparing board meetings) without specifying in advance the time to be spent.

There are various types of retainer arrangement, but from a technical viewpoint two types tend to prevail:

●a generalist retainer, under which the consultant follows global results and trends of the client’s business, looking for opportunities for improvement in various areas and feeding the client with new information and ideas;

●a specialist retainer, providing the client with a permanent flow of technical information and suggestions in an area where the consulting firm is particularly competent and advanced (e.g. computer systems, quality management, international financial operations, identification of new markets).

Another alternative used in some technical assistance programmes is a framework contract.12 In this case the consultant is contracted for a certain kind of services over a period of time. Within this framework agreement, specific assignments or missions are requested by the client and agreed upon case by case according to established rules, such as fee rates or consultant profiles, applicable to the whole contract. The negotiation and contracting procedure is thus simplified and accelerated.

There are various other modes of purchasing consultant services for longer periods without defining specific assignments and repeating each time all the phases of a consulting cycle as described above. Consultants may be permanent members of various committees or boards, special advisers to top managers, observers and advisers in management and board meetings, training faculty members and examiners, informal advisers acting as sources of new ideas and sounding-boards, or personal counsellors. Sophisticated clients tend increasingly to use these flexible and often more cost-effective formulas.

25