Problems Facing Banks

Banks are as likely as any other business to suffer the consequences of an economic recession. Their business customers will suffer from falling sales and losses which will reflect in a surge of bad debts as business loans fail to be repaid. Their private customers are unlikely to fare better. For them the problem becomes redundancy and meeting the normal household bills.

The problem is compounded because banking is becoming increasingly international. The banks' customers are not confined to these shores. They are spread across the world. Even the resources of a giant banking group like Midland or National Westminster are not enough to finance oil exploration or the development of satellite communication systems and this explains the growth of banking consortia. Banks from all the developed countries of the world join forces to supply the capital required for some of the most ambitious (and risky) projects. Unless these international ventures are successful the banks are faced with the problem of collecting debts from customers in countries which are often politically unstable. As if this were not enough, the banks in the UK are also confronted with foreign banks which are beginning to look covetously towards our domestic market for financial services.

Another problem for the banks is the increasing competition between our various financial institutions. At one time there was a clear-cut distinction between the banks and the building societies. The building societies collected savings from ordinary members of the public and lent that money to people who wanted to buy their own homes. In the past banks were not interested in such long term loans, but in recent years they have shifted their ground. They are now increasingly prepared to grant loans to house purchasers, and in response the building societies are offering cheque facilities to their own depositors. The result is that the dividing line between banks and building societies is becoming blurred as the competition warms up. The public at large are the beneficiaries.

Technology provides both opportunities and threats to the banking community. Credit cards have made it easier for the public to buy goods and services and in doing so to run up debts which, when converted into formal borrowings, are very profitable from the banks' point of view. Similarly, the cash dispensing units which give customers greater access to their funds are likely to be popular, particularly among «downmarket» customers. However, cash dispensing units are cheaper than cashiers and, while this may increase the profitability of banks, it is also putting pressure on the Staff Departments to review their recruitment policies.

The major clearing banks report that half the cash withdrawn from branches is taken out of cash dispensing machines – dumb bankers as they are called. Ten years ago, for every National Westminster transaction through a cash dispenser, 15 were conducted over the counter. Now the two systems are level-pegging. The banks and building societies are both affected, but hope they will be able to use the staff freed to sell and service more sophisticated products such as insurance, unit trusts and private pension plans.

Section F. Documentation

Translate all the signatures on the documents below.

Here are two common documents associated with banking:

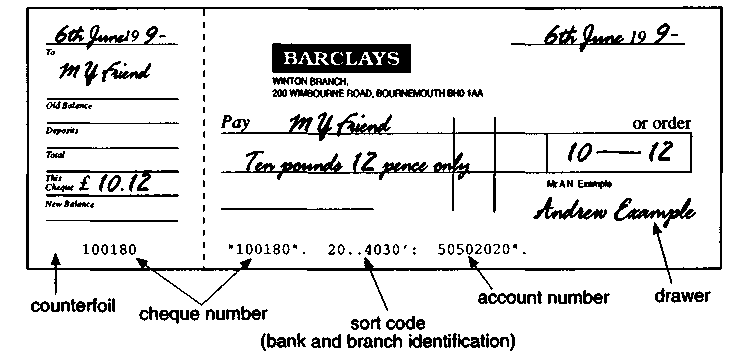

A cheque

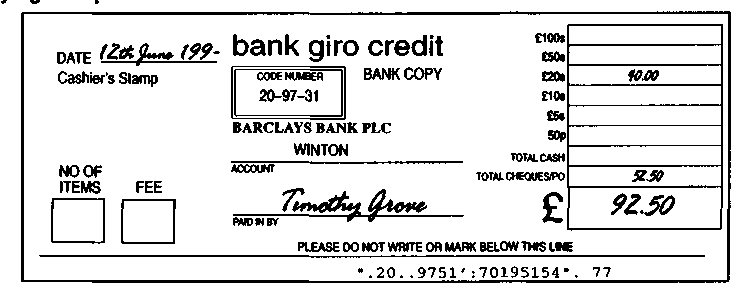

A paying-in slip

Section G. Explanations

Explain carefully the meanings of the highlighted phrases in these sentences.

The customer must exercise reasonable care when giving written instructions, so that the bank is not misled or forgery facilitated.

The bank's duty to repay can be overridden on a countermand of payment by the customer.

When a bank receives notice of a petition to wind up a limited company it will freeze the company's account.

It is a well established practice that bankers will reply to enquiries concerning the financial status* of their customers.

The commercial banks issue travellers cheques which can be cashed at banks all over the world, providing the person tendering the cheque can provide a matching signature to that which appears on the cheque.

Access and Barclaycard, the two main credit cards used in Great Britain, allow the holders to pay for goods or services without cash passing across the counter.

A bank will not usually allow a customer to draw cash against uncleared cheques*.

Section H. Vocabulary

security |

bankrupt |

payee |

application |

building |

authorisation |

Drawer |

credit |

overdraft* |

excess |

mortgagor |

bankruptcy |

guarantor |

liquidity |

principal |

indorsement* |

counterfoil* |

negligent |

central |

confidentiality |

Match the meanings shown below to the words above.

A signature by the payee on the back of a cheque making it transferable.

Complementary part of a bank cheque recording particulars of the payee and the amount paid.

Something deposited or pledged as a guarantee that a loan will be repaid.

The amount by which an overdraft is above the agreed limit.

The capital sum invested as opposed to the interest earned on it.

One of the main duties owed by a banker to his customer.

This society helps people to own their own property.

A situation where assets can be easily converted into cash.

The person to whom a cheque is addressed.

The person who answers for the due fulfilment of a contract.

The right given by a senior official for a subordinate to act.

The person who deposits the deeds of his property as security for a loan.

The side of your bank account on which an entry is made when you pay in.

An act which was carried out without proper care and attention.

The person who signs a cheque authorising the banker to debit his account with the sum in question.

A formal request for a loan or overdraft.

Someone who is unable to pay his debts.

An inability to meet one's commitments may lead to this.

A form of short-term borrowing from a bank.

The Bank of England is this sort of bank.

Section I. Exchange Rates

What would be the effect of the following events on the exchange rate of US dollars in relation to pesetas? Tick the appropriate column.

|

Pesetas would fall in value |

Pesetas would rise in value |

Pesetas would be unchanged |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Section J. Pairs of words

The pairs of words on this list are often confused.

Access (noun) means of reaching

e.g. It is difficult to gain access to the bank's vaults.

Excess (noun) too much of

e.g. The debit balance on the current account was in excess of the overdraft limit.

Affect (verb) to influence or change

e.g. The customer's record will affect the outcome of his application for a loan.

Effect (noun) the resultant change

e.g. If the bank had called for Henry's loan to be repaid the effect on his business would have been disastrous.

Stationery (noun) writing paper and envelopes

e.g. The Securities Clerk, noting that the stationery had run out, ordered some more from Head Office.

Stationary (adjective) not moving

e.g. The bank's security van was stationary when the robbers struck.

Principal (noun) chief/capital sum (adjective) main/leading

e.g. The principal cause of the firm's failure was a lack of working capital.

Principle (noun) one of a set of beliefs

e.g. With regard to loans, banks work on the principle that the borrower must stand to lose as well as the lender.

Your task

Write eight sentences of your own, each of which includes a different one of these words.

Section K. Questions and answers

Read the following questions and then cover them and try to repeat them, one at a time, as accurately as possible. Translate all the questions and answers into Russian. Get prepared to back translating from Russian into English in class.