Ermolaeva_L_D_Ekonomika_i_biznes_1

.pdf2.Which government department is responsible for collecting all the government‟s taxes?

3.Can you give four examples of direct taxes and say something about them?

4.Can you give four examples of indirect taxes and say something about them?

5.What do you know about the direct local tax called “rates”?

6.How does central government spend the money it collects in taxes?

7.Can you give three examples of how local governments spend rate payer‟s money?

XIV. Solve problems through group discussion.

In pairs or small groups discuss:

1)the difference between a progressive and a regressive system of taxation;

2)how the income tax system in Great Britain works.

TEXT В

I. Read the text and try to understand its contents as much as possible.

TAXING BUSINESS IN USA

Businesses are subject to many forms of taxes. Corporate profits are subject to a federal income tax at rates up to 46 percent. Taxes on business property are a major source of revenue for state and local governments. And there are special taxes on goods like liquor and tobacco.

Voters dislike high taxes, but at the same time they demand improved public Services. To many politicians, taxing business seems like an easy way to satisfy voters. Economists have long pointed out, however, that the true burden of all taxes, including taxes on business, falls on people. The people who bear the burden of business taxes are either the firm‟s owners or their customers. If the taxes are passed along to customers in the form of higher prices, they cause inflation. If the burden falls on owners – less innovation, and fewer jobs.

Business taxes not only give government a source of revenue; they also are a way of getting business to do certain things that the government wants done. Firms that invest in new equipment may defer part of their corporate income taxes. This policy is meant to spur investment and job creation. Business climate

71

of states and communities varies widely in terms of taxes. Often states and communities bid against one another in offering tax concessions to companies looking for locations for new plants. Sometimes the bidding takes place on an international scale. The governments have special tax incentives to attract firms in order to provide jobs and raise incomes in their countries. One of the jobs of managerial accountants is to advise firms on how to benefit from tax incentives in making their investment, location, and production decisions.

Notes to the text: |

|

burden |

- бремя |

to bear |

- нести |

to defer |

- отсрочить, отложить |

to spur investment |

- стимулировать вложение |

to bid |

- делать конкурентное предложение |

1.What is a major source of revenue for state and local governments?

2.On whom does a burden of taxes on business fall? How can you explain this?

3.What are the results of raising taxes on business?

4.What other purposes can the government achieve by using the policy of business taxing?

5.Whose job is to advise firms on how to benefit from tax incentives?

TEXT C

I. Translate the text in a written form.

THE OBJECTIVES OF TAX POLICY

Many objectives attributed to tax policy in most countries are really those of public policy as a whole. Economic growth, internal and external stability, and. the attainment of an appropriate distribution of income and wealth fall into this category. Since taxes are one of the most important instruments of government policy in any economy, the effect of taxation on such general public policy objectives as growth, distribution and. stability should be taken into account in designing the tax system.

Growth

An important policy concern in most countries, for example, is the rate of economic growth. The most obvious “growth” objective for tax policy is to provide the resources needed for public sector capital formation and other development related expenditures. The desire to increase and direct private investment may also shape the design of business income taxes in general. Higher taxes may be imposed on retained profits than on distributed profits in order to encourage distribution, the development of capital markets, and the flow of sav-

72

ings to highest-return investment opportunities. Alternatively, higher taxes may be imposed on distributed profits than on retained profits in order to encourage the retention and reinvestment of profits where they are earned.

Distribution

The role of taxation in achieving other public policy goals may often conflict with growth. Tax concessions to investment may raise the rate of growth in certain situations but only at the cost of increasing the inequality with which wealth and income is distributed on the other hand, sometimes measures aimed at one objective may simultaneously move a society towards another. Heavy taxes on land, for example, may induce more efficient utilization of existing assets and raise the level of output while at the same time reducing inequality.

The connection between the distribution of income and the rate of income growth has sometimes been considered to be a simple matter. Economic growth may be viewed as a function of the rate of investment, which must be matched by savings. Since it is well known that the rich save more than poor, the saving “instinct” may need considerable stimulation in the form of low taxes on the rich, and such policies may build up problems for the future. Other countries where the rich spend rather than save, may find redistributive tax policy a more efficient way for producing growth than tax concessions.

Аdministrative limitations suggest to avoid, large, sudden changes in tax structure. Small, regular changes may bе absorbed (accepted.) more easily than large abrupt shifts. There are two main constraints on wealth taxes in most countries: their possible effects on capital flows and. the difficulty of satisfactorily assessing wealth.

Stabilization

The characteristic of the tax system relevant to price level and balance of payments stability is its “elasticity” with respect to changes in the level of income. The more elastic the tax system, the less the need to rely on deficit financing.

Properly structured taxes can help loosen both the immediate and the longterm constraint on growth and more taxes will be needed to transfer increasing real resources to the public sector or through the public sector to private investment.

The suitability of tax elasticity depends not only on economic considerations but also on basic questions of policy.

Notes to the text: |

|

attribute |

- приписывать чего-либо, относить к чему-либо. |

attainment |

- достижение |

concern |

- забота |

to shape |

- сформировать |

73

UNIT VIII

Grammar: Simple, Compound, Complex Sentences.

I. Read and memorize the following words and word combinations:

accounting |

- бухгалтерский учет |

accounts |

- учетно-отчетные документы, документация |

to aggregate |

- собирать в одно целое |

in accordance with |

- в соответствии с |

assets |

- активы, основные средства |

fixed capital assets |

- недвижимость |

allowance |

- скидка или надбавка с учетом чего-либо |

balance sheet |

- балансовый отчет |

bookkeeping |

- бухгалтерия, счетоводство |

capital |

- уставной фонд, капитал |

working capital |

- оборотный капитал |

to cease |

- прекращать |

costs (pl.) |

- расходы, издержки |

cost of average stock |

- стоимость среднего объема продаж |

depreciation |

- физический, моральный износ оборудования, |

|

- скидка на порчу товара, |

|

- снижение стоимости |

debtors |

- дебиторы, дебиторская задолженность, дебет |

double entry |

- двойная бухгалтерия, система двойной записи |

to evaluate |

- оценивать, устанавливать |

fittings (pl) |

- оборудование |

identity |

- идентичность, тождественность, аналогичность |

liabilities |

- пассивы, денежная задолженность, долги |

Ledge |

- гроссбух |

General Ledge |

- главная гроссбух |

maintenance |

- поддержание, содержание счета |

net profit |

- чистая прибыль |

relevant |

- относящийся к чему-либо |

report |

- отчет |

ratio |

- коэффициент |

record |

- учет, регистрация |

accounting record |

- бухгалтерский учет |

to keep records |

- вести учет |

regulation |

- инструкция, устав |

|

74 |

spares |

- запасы, резервы |

stock (pl) |

- ценные бумаги; капитал торговой фирмы, запас |

|

товаров |

in stock |

- иметься в запасе (наличии, ассортименте) для |

|

продажи |

closing stock |

- конечный запас |

opening stock |

- начальный запас |

shop property |

- помещение магазина |

in general terms |

- в общих чертах |

till |

- касса |

turnover |

- оборот |

gross turnover |

- валовый оборот |

term |

- срок |

short term |

- краткосрочный |

value |

- объем, величина |

van (vantage) |

- выгода, прибыль, товары на складе |

to verify |

- проверять, контролировать |

II. Translate the following pairs of words paying attention to the prefix sub-. Use a dictionary if it is necessary:

class – subclass; committee – subcommittee; account – sub-account; station

– substation; agency – sub-agency; division – subdivision; contract – subcontract; company – sub-company; family – subfamily.

III. Add prefix interto the following words and translate them using the dictionary.

change, national, dependent, state, action, connection, departmental, library, related.

IV. Read the international words and guess their meanings:

synthetic, analytical, to summarize, activities, aspect, to synthesize, to combine, a series, regulations, management control system, detailed analysis, balance, analyst, periodicity, memorandum, identity, document.

V. |

Translate the following word combinations with the word “hand” using |

||

|

a dictionary: at hand, on hand, by hand, out of hand, off hand, on the |

||

|

one hand, in hand. Complete the sentences choosing the proper word |

||

|

combination. |

|

|

1. |

I‟ll send you this document tomorrow... |

|

|

|

at hand |

on hand |

by hand |

2. |

I offered him this job, but he refused ... |

|

|

|

|

|

75 |

by hand out of hand off hand

3. You‟ II have to be strict with your subordinates, they very quickly get...

on hand out of hand on the one hand

4.You are asking when we visited this company? Oh, dear, I can‟t remember… .

|

off hand |

in hand |

out of hand |

5. |

The examinations are… |

|

|

|

off hand |

at hand |

out of hand |

6. |

We have some new goods… |

|

|

|

in hand |

off hand |

on hand |

7. The work is … but not finished. |

|

||

|

out of hand |

in hand |

off hand |

VI. Translate the sentences paying attention to different meanings of the word “stock”.

1.Stock is a store of goods for use when needed.

2.Sometimes stock means the capital of a business company, often divided into units, giving the holder a right to a share in the profits.

3.Store inventory reduces producer‟s need to carry large stocks.

4.He has £500 in stocks.

5.My family invested money in railway stocks.

6.The firm has 100 articles in stock at the beginning of the year.

7.In order to increase its market share the company renewed its stock.

VII. Point out the types of clauses in each of the following sentences and indicate (circle) the words they are related to.

1.Before the person pays income tax to the government he is allowed to deduct allowances for expenses that he has had to pay during the year.

2.That accounting is the establishment, maintenance, collection and analysis of financial records every businessman must know.

3.Accounting is used to provide data on any changes that have occurred, or that may occur, over time.

4.Although the financial statements are basically addressed to the external constituencies of an enterprise, these reports are also used by enterprise managers.

5.Hoarding advertisements are put up at the side of the road so that everyone could see them clearly.

6.The suggestion was that the financial report of the organization must be made without delay.

76

VIII. Group the sentences into simple, compound, and complex and translate them.

1.Management will need to learn how to use accounting information for managerial decision making.

2.I realized he was displeased with the financial statement.

3.If the financial reports are for internal use the accounting period is usually either a week or a month.

4.The manual workers in Great Britain do not like to change their job location, and this leads to a lot of unemployment in some areas.

5.If the company does well then the interest paid to the shareholders will be high, but if the company does not make a profit then it may pay no dividend at all to the shareholders.

6.In accounting, capital means the total financial assets of an organization whether in the form of money, property, goods or equipment.

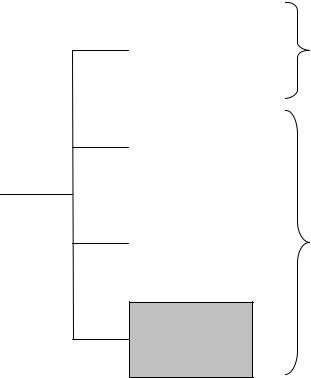

TEXT A

ACCOUNTING

Accounting is the language of business. Accounting shows a financial picture of the firm. Accounting reports on the effects of the transactions on the firm‟s financial condition. Accounting records give a very important data. It is used bу management, stockholders, creditors, independent analysts, banks and government.

The accounting process has four main stages. Detailed rules and regulations need to be followed at each stage of the accounting process.

77

Financial and Managerial Accounting |

|

|||

|

|

|

|

|

|

|

|

Information |

Managerial |

|

|

|

for |

|

|

|

|

Accounting |

|

|

|

|

Management |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Public |

|

|

|

|

Financial |

|

|

The |

|

Statements |

|

|

|

|

|

|

|

Accounting |

|

|

|

|

Process |

|

|

Financial |

|

|

|

Tax Returns |

|

|

|

|

||

|

|

|

Accounting |

|

|

|

|

|

|

|

|

|

|

|

Special Reg-

ulatory

Reports

Figure 6. Financial and managerial accounting

At the first stage, business transactions are documented. In the second stage accounting data is aggregated. The system of aggregation usually involves the maintenance of a series of interrelated synthetic accounts (first-order accounts), sub-accounts (second-order accounts), analytic accounts and memorandum accounts. The sub-accounts combine the data which are contained, in a particular group of analytic accounts and. are then summarized in the relevant synthetic accounts. The synthetic accounts “synthesize” the enterprise‟s activities. The analytic accounts provide a more detailed analysis of these activities and. are usually designed by the chief accountant of the enterprise in accordance with the need for proper bookkeeping. The memorandum accounts are used for detailed, recording of events outside the double-entry system. As a rule, only synthetic accounting records without sub-accounts are entered in the General Ledger; necessary data on sub-accounts and analytic accounts (cash books, etc.) are kept in the ledger registers. The identity of the analytic accounting data, and the turnover and balances in the synthetic accounts must be verified on the first day of each month.

78

At the third stage, accounting reports are prepared. The forms contents, and periodicity of various types of reports depend on the requirements of the state financial reporting system.

At the final stage, analysis of business activities of an enterprise is carried out. The analysis, called “economic analysis”, is an important aspect of management control systems in our enterprises. The results of analysis are used for management decision-making and performance evaluation of the enterprise (fig. 6).

IX. Find definitions to the terms given in the left column.

1) report |

a) a person who keeps accounts in a business |

2) turnover |

b) one of the principal books in which accounts are kept in |

|

a business house |

3) balance sheet |

c) a detailed account after investigation |

4) ledger |

d) the amount of money involved in business operation |

|

within a given time |

5) accountant |

e) a number of separate things brought together into a mass |

|

or group |

6) aggregation |

f) a written statement of money paid and received |

X. Answer the following questions using the information of text A.

1.How many stages are there in the accounting process?

2.What is done in every stage?

3.What can you say about aggregation?

4.What is the difference between synthetic accounts and analytic accounts?

5.What do we use the memorandum account for?

6.What is carried out at the final stage of the accounting process?

7.Where is the economic analysis used?

XI. Fill up the scheme and speak about the accounting process. The four stages of accounting process.

I |

|

II |

|

|

III |

|

|

|

IV |

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Business |

Accounting |

transactions |

reports |

79

XII. Accountants communicate financial information to many people. Look at the figure and say:

1.What branches of accounting are there?

2.Which type of accounting provides information for use inside and outside the firm?

3.Who uses each type of financial accounting? Use the hints in brackets (investors, customers, suppliers, federal governments, local governments, government regulatory agencies).

XIII. Read and translate the following dialogue. Act out the dialogue in pairs.

A.: Glad to meet you. You look very busy. There were so many statements on your table.

B.: This is the end of the year. The accounting department is very busy. A.: So, how‟s business?

B.: I don‟t know everything. I am busy with some records and statements. I don‟t have the whole picture. But I think the company is doing very well.

A.: I am sure of it.

B.: Well, the balance sheet and profit and loss statement are assets and liabilities, net worth and profit position of the company in the financial statements.

A.: Thank you for information. B.: Oh, it‟s my pleasure.

XIV. Read and translate the following dialogue. Act out the dialogue in pairs.

THE BUDGET MEETING

P.: Right, let‟s get started. Now you‟ve all seen the budget proposals for next year. Have you got anything to say?

J.: I think the research figure is too low. We should increase it by at least 5%. P.: Well, we could do that, but it means less money for the other departments. I

think it should stay the same.

S.: I agree with John. We could reduce the figure for marketing – that would allow us to increase the budget for research.

P.: I felt marketing needed a good figure this year. They‟ve got a big launch, mid-year. I think they couldn‟t manage with less.

J.: I‟m sure they could.

80