3. Estimation of non-material assets

The estimation (definition of the cost of non-material assets) depends on the way of their purchase. Non-material assets can be brought as the contribution into authorized capital stock (chartered capital), purchased from other organizations, received free of charge, created at the enterprise itself. Therefore the estimation can be made by the arrangement of the parties, proceeding from expenses for purchase, at market cost, at manufacturing cost.

Acquisition cost of purchased non-material assets is defined as the sum of all actual charges for the purchase and their putting into the state, which is suitable for use for the planned purposes.

For estimating non-material assets it is possible to use three basic approaches: profitable; cost-based; comparative.

According to the profitable approach the cost of an object of non-material assets is accepted at the level of the current cost of those advantages which the enterprise has from its use. As an example it is possible to adduce the method of clearing of royalty which is used for estimating cost of patents and licenses. Royalty is a periodic deduction to licensor (seller) for using the intellectual property. Usually royalty makes 5-20 % of additional profit received by the enterprise which has bought the intellectual property. If the object of the intellectual property is the basis of a new product (technology), royalty can make up to 50 %.

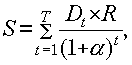

In case when the invention is purchased on the basis of royalty the cost of the license for using the invention is equal to discounted stream of royalty:

where Dt

-

rate of royalty;

R

- basis of calculating royalty (proceeds from production which is put

out by the license, or the profit received from realization of

corresponding production); Т

-

term of validity of the license contract;

t

– an ordinal number of the year under review;

![]() -

the rate of discount.

-

the rate of discount.

When using the cost-based approach non-material assets are estimated as the sum of expenses for their creation, purchase and introduction (input).

The comparative approach can be applied to those kinds of non-material assets, transactions with which are frequently made at the market. Sale prices for analogous objects serve as initial information for calculating the cost of an object.

4. Depreciation of non-material assets

Non-material assets are taken into account on accounting balance at residual cost. The cost of objects of non-material assets is repaid by charge of depreciation during the fixed term of their paying usage. Depreciation charges are made by one of the following methods:

- by the linear method proceeding from the norms set by the organization on the basis of term of non-material assets paying usage;

- by the method of diminishing residue;

- by the method of writing off the cost in proportion to the volume of production (work, services).

Application of one of methods for a group of homogeneous non-material assets is carried out during the whole term of their paying usage.

The term of paying usage of non-material assets is defined by the organization when taking the object onto the balance. The term of paying usage is the period during which the use of the object brings profit, benefit to the enterprise.

The term of paying usage for patents, licenses, rights of usage and so on is the term which is stipulated by the contract.

Depreciation is not charged from non-material assets received by the contract of donation and free of charge in the process of privatization, obtained with usage of budgetary appropriations, and from non-material assets of budget organizations.

There is an opportunity not to charge depreciation charges from some kinds of non-material assets the list of which the enterprise establishes independently. Usually assets the cost of which does not decrease in the course of time (for example, trade marks) belong to them.

Depreciation charges from non-material assets begin with the first date of the month which follows the month of accepting this object onto the balance, and are charged till the complete repayment of the cost of this object or withdrawal of this object from the balance. Depreciation charges from non-material assets stop from the first date of the month which follows the month of the complete repayment of the cost of this object or writing off this object from the balance.