03b_И_debate

.pdfMANAGEMENT

Applied Summer School

Business in Europe

A Single European Currency – A Debate

Prof. Vito Bobek

University of Apllied Sciences FH Joanneum

vito.bobek@fh-joanneum.at

MANAGEMENT

Key Issues

•Why to have convergence criteria?

•What are the basic effects of a single currency?

•What are the motivations for joining the Euro?

•The case for EMU entry

•The case against EMU entry

•Optimal currency areas

•Tensions for the single currency in 2009-2010

MANAGEMENT

Basics on the Euro

•A single currency requires a common interest rate for the Euro Zone – i.e. a common monetary policy

•17 member nations are inside the Euro Area

•The European Central Bank (ECB) sets official interest rates to meet an inflation target of 2%

•The approach of ECB is different to that of the USA Federal Reserve (dual target)

•The US Federal Reserve tends to set interest rates to maintain growth and avoid deflation.

MANAGEMENT

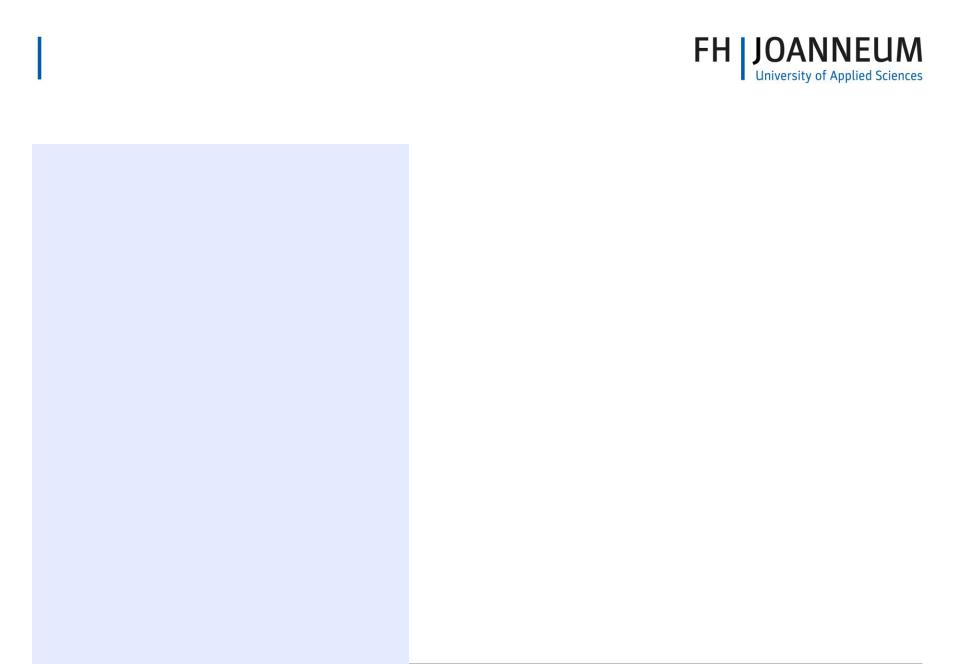

Euro Zone Interest Rates

Percent

Interest Rates for the Euro Area and for the UK

Per Cent

8.0 |

|

8.0 |

|

Bank of England Rates

7.0

7.0

7.0

6.0 |

|

|

|

|

|

|

|

|

|

6.0 |

5.0 |

|

|

|

|

|

|

|

|

|

5.0 |

4.0 |

|

|

|

|

|

|

|

|

|

4.0 |

3.0 |

|

|

|

|

|

|

|

|

|

3.0 |

2.0 |

|

|

|

|

|

|

|

|

|

2.0 |

Euro Zone Interest Rates |

|

|

|

|

|

|

|

|

||

1.0 |

|

|

|

|

|

|

|

|

|

1.0 |

0.0 |

|

|

|

|

|

|

|

|

|

0.0 |

99 |

00 |

01 |

02 |

03 |

04 |

05 |

06 |

07 |

08 |

09 |

Source: Reuters EcoWin

MANAGEMENT

Judging the Success of the Euro

•The Euro project should be judged according to whether it achieves its long term aims:

1.Sustained non-inflationary growth

2.Lower long-term interest rates and higher rates of investment

3.Lower unemployment

4.Expansion of the EU single market

•The Euro on its own in insufficient to achieve these – structural economic reforms in Europe are also required and many are taking place.

MANAGEMENT Nominal v Real (Structural)

Convergence

Nominal Economic Indicators

•(Those required under the Maastricht Treaty)

•Consumer price inflation

•Short term interest rates

•Fiscal (Budget) deficit

•Gross government debt

•Exchange rate stability

MANAGEMENT

Nominal vs. Real (Structural) Convergence

Nominal Economic Indicators

•(Those required under the Maastricht Treaty)

•Consumer price inflation

•Short term interest rates

•Fiscal (Budget) deficit

•Gross government debt

•Exchange rate stability

Real Economic Indicators

•(Important in the long term)

•Trend growth of GDP

•Labour market performance

•Trend growth of labour productivity

•Trade balances in goods and services

•Investment/GDP ratios

•Housing market structure.

MANAGEMENT

Is the Euro an Optimal Currency Zone?

•An optimal currency zone occurs when:

–(1) Countries have achieved real convergence

–(2) They respond in similar ways to external economic shocks or macro policy changes

–(3) They have sufficient flexibility in both their product markets and labour markets to deal with these shocks

•High geographical mobility of labour

•High occupational mobility of labour

•Wage and price flexibility in factor markets

–(4) Countries are prepared to use fiscal transfers to even out some of the regional economic imbalances within the European currency union

MANAGEMENT

Optimal Currency Zones (2)

•By most criteria, the current Euro Zone does not come close to an optimal currency zone!

–The core group of EU countries are broadly similar (Germany + France + Netherlands + Belgium)

–But peripheral countries have big structural differences

–And there are barriers to the mobility of labour

–Little wonder that tensions are rising in the Euro Area as recession bites

MANAGEMENT

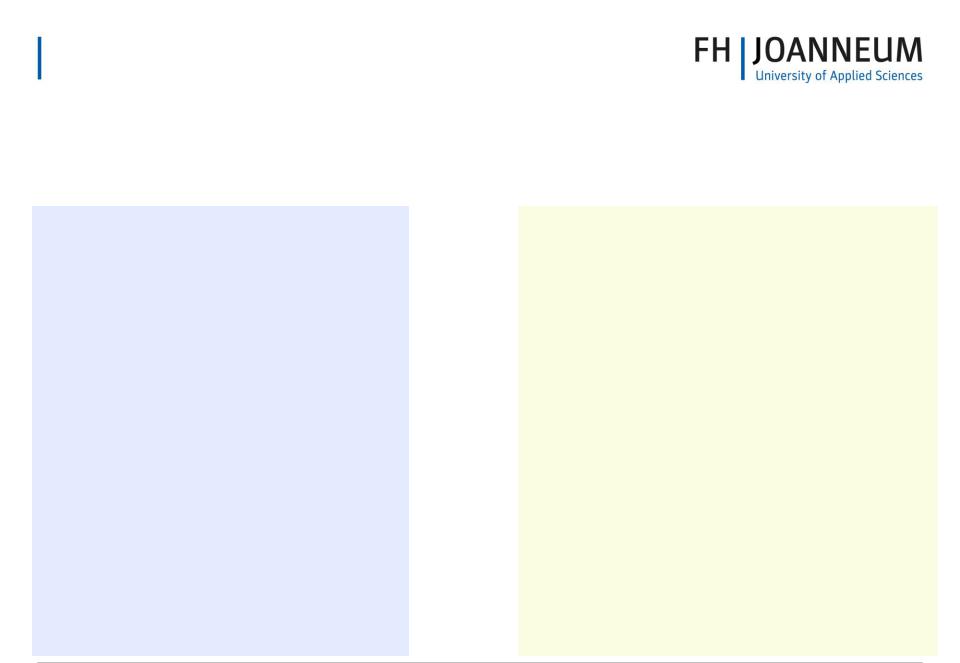

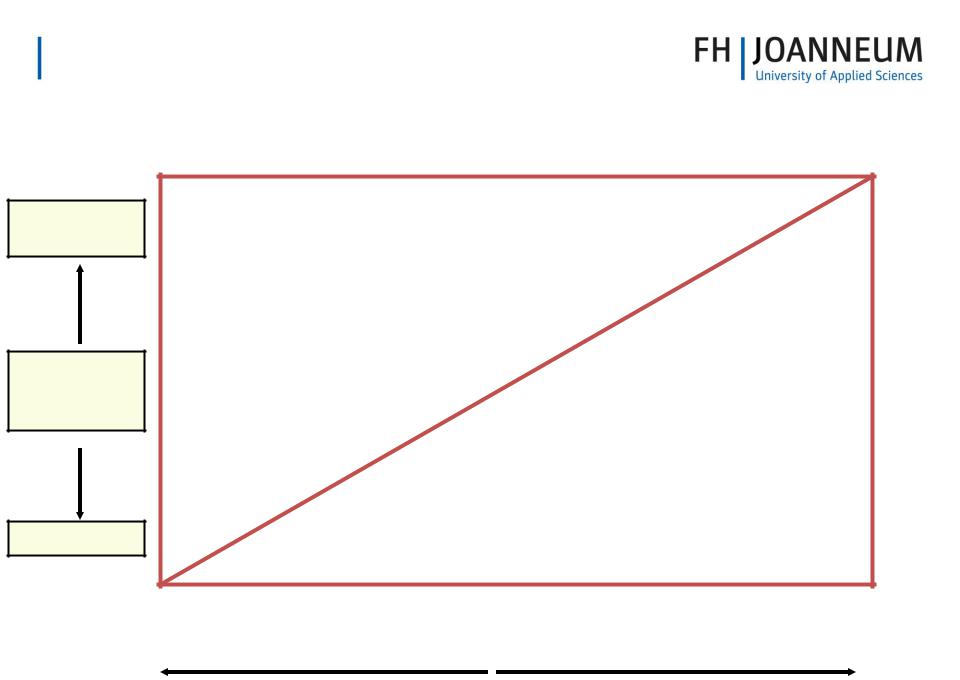

Optimal Currency Zones

Highly

Flexible

Labour

Market

Flexibility

Inflexible

|

Divergent |

|

Real Economic Convergence |

|

Convergent |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|