CFA Level 1 (2009) - 3

.pdf

Srudy Session

Cross-Reference to CFA Institute Assigned Reading 1135 - Inventoril

LOS 35.e

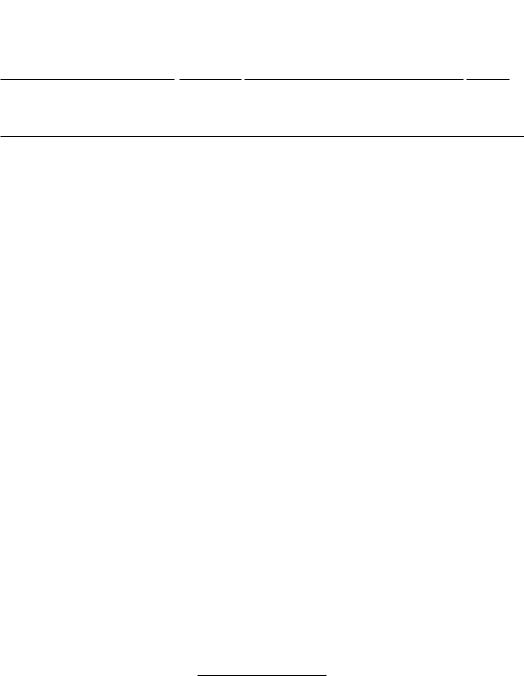

I When prices arc rising and inventory quantities arc stable or increasing:

UFO rl'wlrf.)w |

FIFO rnlllrs ill: |

higher COCS |

lower COCS |

lower taxes |

higher taxes |

lower net income |

higher net income |

lower inventory balances |

higher inVl'ntOfy balances |

higher cash Hows (less taxes paid out) |

lower Clsh Hows (more taxes p~lid out) |

lower net Jnd gross margins |

higher net and gross margins |

100\!er current ratio |

higher current ratio |

higher inventory turnover |

lower inventory turnover |

DfA and DIE higher |

DfA and DfE lower |

\VeiglHcd :lverage COSt provides results berween LIFO and FIFO.

LOS Yi.r

For an~J!nical ~lI1d cOlllpHisun purpuses, l.In·) in\'cnwl)' should he cun\l'!tul tu

Fin) invel1lory b)'adding rhc LIFO reserve ro currelH assets, "dding incumc LlxeS un rhe UFO resel"\'e to current liabilities, and adding the UFO reserve, ner of rE, to stockholders' equity, so thar rhe accouIHing equation b~J!ances. LIFO COGS can

he convened ro FIFO COGS by subrracring rhe change in rhe LIFO resl'!VC over rhe period.

LOS Yi.g

The LIFO reservc can decline because of eirher ~I UFO liquidarion or falling pricl'S, A UFO liquidation (in\"C'nrory quantity deCleases) will resulr in lower COGS and an increasc in !1roht as older, lowC/-cost inventor)' is (assuilled to he) sold. H()\\'cv('r, thc inClC;\se in profit is ;\[rihcia\ (phantom) because it is nor susrainable once the c'llrrent

inn:ntl1l)' is depletcd. \,\'hen fJrices are decreasing, inventor), v~lllle is higher under UFO LlLII1 under FIFO, so rhe UFO resnvc declines.

©2008 Kaplan Schwncr