Economics_-_New_Ways_of_Thinking

.pdfThe money supply consists of currency, checking accounts (balances), and traveler’s checks. The amounts shown represent the money supply in August 2005.

savings account

An interest-earning account.

near-money

Assets, such as nonchecking savings accounts, that can be easily and quickly turned into money.

checking accounts, and $7 billion in traveler’s checks. Altogether, the money supply equaled $1,336 billion (see Exhibit 10-2).

You might be wondering why debit cards aren’t mentioned; after all, you can buy products with a debit card in the same way that you can with currency. Do you see why the debit cards aren’t included in our list? They are already represented in checking accounts. When you use a debit card, money is removed from your checking account in the same way that it is when you write a check.

Another card that some people might in the future think of as currency are smart cards. A smart card resembles a credit card in shape and size, but it is not just a simple piece of plastic the way a credit card is. Inside it is an embedded 8-bit microprocessor. A smart card can be used for many things, and it can hold significant amounts of data. For purposes here, though, we need to point out that a monetary value can be placed on a smart card (much like a monetary value can be placed on a card at a video arcade), and then the card can be used to make on-the-spot purchases, much like currency is used for the same thing.

QUESTION: I am used to thinking that only the cash and change I have in my wallet is money. Are we saying cash is only one component of money?

ANSWER: Yes, that is exactly what we are saying. Remember that money is anything that is widely accepted in exchange and in the repayment of debt. The cash and change in your wallet (the currency in your wallet) is widely accepted in exchange and in the repayment of debt, so it is money. The check you might write out for $100 is also accepted in exchange and in the repayment of debt, so it is money. Traveler’s checks are also widely accepted in exchange and in the repayment of debt, so they are money too. In summary, money consists of currency plus checking accounts plus traveler’s checks.

Is a Savings Account Money?

A savings account is an interestearning account. For example, if you have $400 in your savings account and the annual interest rate you are paid is 6 percent, in a year your savings account will increase to $424. With some savings accounts, you can write checks; others you cannot. Savings accounts on which you can write checks fall into the category of checking accounts, which were discussed earlier. A passbook savings account is an example of a nonchecking savings account. When you deposit your money into a passbook savings account, you are given a small booklet in which deposits, withdrawals, and interest are recorded.

A nonchecking savings account is not considered money because it is not widely accepted for purposes of exchange. No person can go into a store, show the salesperson the balance in a passbook savings account, and buy a $40 sweater. However, nonchecking savings accounts are considered near-money. Near-money is anything that can be relatively easily and quickly turned into money. A person cannot buy a sweater by telling the salesperson that she has so much “money” in her passbook savings account, but she can go to the bank and request that her nonchecking savings be returned to her in currency (“I’ll take it in twenties”).

264 Chapter 10 Money, Banking, and the Federal Reserve System

The money supply has been increasing in the United States over time. The following table shows the money supply figures for the years 1989–2005. (The figure for 2005 was reported in August 2005.) All numbers are in billions of dollars. Is the money supply in a following year always higher than the money supply in a prior year? If you want to find the most recent money supply figures, you can go to www.emcp.net/federalreserve and click

on Table 1.

|

Money supply |

Year |

(billions of dollars) |

1989 |

$ 793 |

1990 |

825 |

1991 |

897 |

1992 |

1,025 |

1993 |

1,129 |

1994 |

1,150 |

1995 |

1,126 |

1996 |

1,079 |

1997 |

1,072 |

1998 |

1,094 |

1999 |

1,122 |

2000 |

1,087 |

|

|

2001 |

1,179 |

2002 |

1,216 |

|

|

2003 |

1,299 |

2004 |

1,367 |

|

|

2005 |

1,336 |

|

|

Are Credit Cards Money?

You’re out on a Friday night with your friends eating pizza. Someone asks, “Anyone here got any money?”You say,“I have a credit card.” Your friends say, “Good enough.”

Is a credit card money? After all, it is often referred to as “plastic money,” and most retailers accept credit cards as payment for purchases. On closer examination, we can see that a credit card is not money.

Consider Tina, who decides to buy a pair of shoes. She hands the shoe clerk her Visa card and signs for the purchase. Essentially, what the Visa card allows Tina to do is take out a loan from the bank that issued the card. The shoe clerk knows that this bank has, in effect, promised to pay the store for the shoes. At a later date, the bank will send Tina a credit card bill. At that time, Tina will be required to reimburse the bank for the shoe charges, plus interest (if her payment is made after a certain date). Tina is required to discharge her debt to the bank with money, such as currency or a check written on her checking account.

Can you see that a credit card is not money? Money has to be both widely used for exchange and be used in the repayment of debt. A credit card is not used to repay debt but rather to incur it. It is an instrument that makes it easier for the holder to

Today, if you have near-money, you can quickly and easily turn it into money, either at the bank or through your online banking service. What is near-money?

Section 2 The Money Supply 265

WhatIsMoney |

||

??? |

||

inaPrisoner |

of |

|

War |

Camp? |

|

|

|

|

During World War II, an

American, R. A. Radford, was captured and imprisoned in a prisoner of war (POW) camp. During his stay, he noted that the Red

would periodically distribute to the prisoners packages that contained goods such as cigarettes, toiletries, chocolate, cheese, margarine, and tinned beef. Not all the prisoners had the same preferences: some liked chocolate but did not like cigarettes, whereas others liked ciga-

Cigarettes were money in prisoner of war camps.

rettes but did not like cheese. Soon, the prisoners began to barter-trade with each other. One prisoner, who had cigarettes and wanted more chocolate, would try to find another prisoner who wanted less chocolate and more cigarettes.

As this chapter explained, barter is a more time-consuming and difficult way to trade than trading with money. Soon the prisoners no longer bartered goods; they used money instead. The money was not U.S. dollars, French francs, German marks, or British pounds. In fact, it was not any national money at all; cigarettes emerged as the money in the POW camp. They were widely accepted for purposes of exchange. Soon chocolate bars, cheese, and other goods were quoted in “cigarette prices”: 10 cigarettes for a chocolate bar, 20 cigarettes for cheese, and so on.

THINK Why did the cigarette ABOUT IT rather than the choco-

late or cheese become money?

loanable funds market

The market for loans. There is a demand for loans (stemming from borrowers) and a supply of loans (stemming from lenders). It is in the loanable funds market where the interest rate is determined.

a person in debt, which he or she then has to repay with money.

Don’t think of the card as money because it isn’t money. Think of it as what it is—a piece of plastic that allows you to take out a loan from the bank that issued the card.

In other words, when you hand the credit card to the cashier to pay for the pizza, or shoes, or new CD, it is you and the bank standing up there in front of the cashier—not just you alone. The bank is saying to you, “Here, we are going to lend you some ‘money’ to pay for the item. Oh, and by the way, we want you to pay us back later, with interest.”

To get a better understanding of credit cards, turn to page 268 and read about “The Psychology of Credit Cards” in the “Your Personal Economics” feature.

Interest Rates

As you know, when a person uses a credit card, he or she is actually borrowing funds from a bank. In other words, the person is a borrower and the bank is a lender. Often, when loans are made, an interest rate must be paid for the loan.

Now if we look at interest rates (for loans) over time, we see that sometimes interest rates are higher than at other times. For example, in the 1970s, interest rates were relatively high. In 2004, interest rates were relatively low.

Why are interest rates high at some times and low at other times? The answer has to do with supply and demand, which you learned about in Chapters 4 through 6. Interest rates are determined in the loanable funds

266 Chapter 10 Money, Banking, and the Federal Reserve System

Credit cards are not money—they cannot be used to repay debt. What is the relationship between credit cards and debt?

market in much the same way that apple prices are determined in the apple market, computer prices are determined in the computer market, and house prices are determined in the housing market.

The loanable funds market includes a demand for loans and a supply of loans. The demanders of loans are called borrowers; the suppliers of loans are called lenders. Through the interaction of the demand for and supply of loans, the interest rate is determined.

What happens if the demand for loans rises? Obviously, if the demand for loans rises and the supply remains constant, the price of a loan, which is the interest rate, rises. What happens if the demand for loans

falls. What happens if the supply of loans falls? The interest rate rises.

Sometimes people make a distinction between short-term interest rates and longterm interest rates. The terms short and long refer to the time period of the loan. For example, if you were to

take out a six-month loan, it would likely be referred to as a shortterm loan, in contrast to, say, a 30-year loan, which would be referred to as a

long-term loan. The interest rate you paid (as a borrower) for the six-month loan would be referred to as a short-term interest rate; the interest rate you paid for the

Defining Terms

1.Define:

a. money supply b. currency

c. Federal Reserve note

d.demand deposit

e.savings account

f.near-money

Reviewing Facts and

Concepts

2.What is the official name for a “dollar bill”? (Hint:

Look at a dollar bill and see what is written at the top.)

3.What is the difference between near-money and money?

Critical Thinking

4.Credit cards are widely accepted for purposes of exchange, yet they are not money. Why not?

Applying Economic

Concepts

5.Take a look at a Federal Reserve note. On it, you will read the following words: “This note is legal tender for all debts, public and private.” What part of the definition of money does this message refer to?

Section 2 The Money Supply 267

The Psychology of Credit Cards

If you work to earn $50, do you use the money in the same way

that you would use a $50 gift? Many economic studies show that people often are more serious with money they earn than with money they win or receive as a gift. In reality, a dollar is a dollar is a dollar, no matter from where it came. But in everyday life, we see a dollar earned as somehow different from a dollar won.

$100 “Out the Window”

Suppose you plan to go to a concert, and the ticket costs $100. You buy the ticket on Monday to attend the concert on Friday. When Friday night comes, you realize you lost the ticket. Assuming that tickets are still available, do you buy another? Answer the question before reading further.

Now let’s change the circumstances. Suppose instead of buying the ticket on Monday, you plan to buy it on Friday, right before the con-

If you lost your ticket to this concert, would you buy another?

cert. At the ticket window on Friday night, you realize that on your way to the concert you lost $100 out of your wallet. You brought plenty of money so you still have enough to buy the ticket. Do you buy it?

The Economist Says…

According to economists, the two settings present you with the same choice. In both settings, you have to spend another $100 to see the concert. Because the two settings present you with the same choice, economists argue that you will behave the same in the two settings. If you decide not to buy another ticket in the first setting, then you shouldn’t in the second. If you do decide to buy another ticket in the first setting, then you should in the second.

But in Real Life…

People don’t seem to behave the way that economists predict, however. Many people, when asked the two questions in this example, say that they will not buy a second ticket if they lost the first ticket, but they will buy a ticket if they lost $100. Why? These people argue that spending an additional $100 on an additional ticket is like spending $200 to see the concert, which is too much to pay. However, they don’t see themselves spending $200 to see the concert when they lose $100 on the way to the concert and pay $100 for a ticket. To these people, the situations are completely different.

Economists say that the people who answer the two questions differently—although both settings offer the same basic choice—are compartmentalizing. They are treating two $100 amounts differently, as if they come from two different compartments. The concert ticket example shows that people do compartmentalize when it comes to money. They don’t always treat a dollar in the same way.

Cash Versus Credit Cards

With this example in mind, let’s compare using cash to using a credit card. Say a person has $500 in cash and a credit card in her wallet. She wants to purchase something that costs $480. She could use the cash to make the purchase, or she could put the purchase on her credit card (and pay off the credit card later). In this situation, many people will say that it is somehow easier to use the credit card than to pay cash. When they pay cash, they say, they have a harder time making the decision to purchase the item. Somehow it seems more real to them; somehow the purchase seems more expensive.

You and Your Lending Partner

It may be easier to use a credit card than to pay cash, but it certainly is not cheaper. In fact, it can be more expensive. If you don’t pay credit card balances off monthly, you will end up paying interest on the loan the bank provided you via your credit card purchase.

268 Chapter 10 Money, Banking, and the Federal Reserve System

You must either pay for something when you buy it or pay later. If you pay later, you often pay more.

In a sense, when you buy something with a credit card, two people, not one, stand in front of the cashier making the purchase. First is you, handing over your credit card. Plus, “standing” next to you, is “your partner” representing the bank. This imaginary partner is there with you, issuing you a loan to make the purchase with the credit card. Later, your “ partner” from the bank will come back to you and ask to be repaid for the loan, with interest. In other words, a $100 item will cost you $100 if you pay in cash, but it could cost you $110 if you pay with a credit card ($100 for the purchase and $10 interest paid for the $100 loan).

An Expensive Lesson

Making a credit card purchase might be easier (for you) than a cash purchase of the same denomination, but often it is a costlier purchase. Not realizing this can lead to serious financial trouble, as far too many people have learned the hard way.

Consider Kevin (a real person whose name has been changed). He went off to college with a credit

card. The first two months at college he used the credit card for all his purchases—many purchases. Kevin purchased new clothes, took his friends out to eat regularly, and bought an expensive television for his dorm room.

When Kevin received the credit card bill, he was shocked at just how much he had spent. (It seemed so easy to spend when he was out with his friends having a good time.) He said he felt as if someone else had

spent the money. In his words, “It felt like I was getting things for free.” Now Kevin certainly was smart enough to know that he wasn’t getting anything for free, but he wasn’t stating what he knew, he was telling us how he felt. Looking back, he realized his compartmentalizing caused him to buy a lot more than he would have if he paid in cash. In the end he had to work many more hours (than he had wanted to) to pay off his credit card bill.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Economics |

Action |

Plan |

|

|

|||||||||||||||||||||||||||||||||||||||||

My Personal |

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

and some |

|

|

|||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

you may want |

to consider |

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||

|

|

|

are some |

points |

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||

Here |

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

|

|

|

you might |

want |

|

to put into |

practice |

|

|

|

|

|

|

|

|

|

|

|

are, |

|

|||||||||||||||||||||||||||||||||||||||||

guidelines |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

the holes |

|

|||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

where |

|

|||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

if you know |

|

|||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

said that |

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||

|

|

Someone once |

|

|

|

|

|

this observation |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||

1. |

|

|

|

|

|

|

|

|

|

|

. Does |

|

|||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||

|

|

you are |

less likely |

to step |

in them |

|

|

that credit |

cards |

can |

|

||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

If you know |

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

cards? |

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||

|

|

apply to credit |

|

to get into financial |

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

you are less |

likely |

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

be abused, |

then |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

|

trouble with |

credit |

cards |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

or cash |

until I |

|

|||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

of a check |

|

||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

card instead |

|

|||||||||||||||||||||||||||||||||||||||||||||||||

|

I will not |

use a credit |

|

|

|

|

|

that I am |

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

proven to myself |

|

|

||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

years |

|

old and have |

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||

|

am |

______ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

- |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

financially |

responsible |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

do sometimes |

compartmental |

|

|||||||||||||||||||||||||||||||||||||

|

|

|

|

Keep |

in mind that people |

|

|

|

|

. The truth of |

|||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||

|

|

2. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

always |

a dollar |

|

|

|

|

|

|

|

||||||||||||||||||||||

|

|

|

|

|

. For |

them, a dollar |

is not |

|

|

|

|

|

|

|

|

|

|

A |

|

|

|

||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

themselves: |

|

|

|

|||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||

|

|

|

|

|

ize |

|

|

|

|

|

|

|

|

is, people |

are deceiving |

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

the matter |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

dollar |

is a dollar |

|

is a dollar |

|

|

|

|

|

|

|

|

|

|

|

percent |

of money |

|

||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

______ |

|

|||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

I will spend |

only |

|

|||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||

|

|

In the future, |

|

|

|

|

|

|

. |

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||

|

|

|

and I will save |

______ |

percent |

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||

|

|

gifts |

I receive, |

|

|

|

|

|

|

|

|

that costs |

|

|

|||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||

|

|

|

a credit card |

to buy something |

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

If you use |

|

|

|

|

for the |

|||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

3. |

|

|

|

|

|

|

|

|

|

more |

than $100 |

|||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

may end |

up |

paying |

|

|

|

|

|

|

|

|

|

|

|

|

- |

|||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

$100,you |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

a credit card to |

buy some |

|||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

speaking,using |

|

|

. |

||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

. Generally |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

than |

using cash |

||||||||||||||||||||||||

|

|

|

|

|

|

|

|

item |

|

makes |

that something |

costlier |

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

thing |

|

|

|

|

|

|

|

|

|

|

I will |

||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

I know |

for sure that |

|||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

card unless |

|

||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

not use |

a credit |

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

I will |

|

|

. |

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||

|

|

|

|

|

|

|

to pay my |

|

bill in full when |

it comes |

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

be able |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

Chapter 10 Money, Banking, and the Federal Reserve System 269

The Federal

Reserve System

Focus Questions

What is the Federal Reserve System (the Fed)?

How many persons sit on the Board of Governors of the Federal Reserve System?

What are the major responsibilities of the Federal Reserve System?

How does the check-clearing process work?

Key Terms

Federal Reserve System (the Fed)

Board of Governors of the Federal Reserve System

Federal Open Market Committee (FOMC) reserve account

Federal Reserve System (the Fed)

The central bank of the United States.

Board of Governors of the Federal Reserve System

The governing body of the Federal Reserve System.

What Is the Federal Reserve

System?

In 1913, Congress passed the Federal Reserve Act. This act set up the Federal Reserve System, which began operation in 1914. (The popular name for the Federal Reserve System is “the Fed.”) The Fed is a central bank, which means it is the chief monetary authority in the country. A central bank has the job of determining the money supply and supervising banks, among other things. Today, the principal components of the Federal Reserve System are (1) the Board of Governors, and (2) the 12 Federal Reserve district banks.

Board of Governors

The Board of Governors of the Federal Reserve System controls and coordinates the Fed’s activities. The board is made up of seven members, each appointed to a 14year term by the president of the United States with Senate approval. The president also designates one member as chairperson of the board for a 4-year term. The Board

of Governors is located at 20th Street and Constitution Avenue in Washington, D.C.

QUESTION: Do other countries have a Federal Reserve System?

ANSWER: As stated earlier, the Federal Reserve System is a central bank, and other countries do have central banks. Whereas we, in the United States, call our central bank the Federal Reserve System, in most other countries the central bank is either called “the central bank” or “the bank” of that particular country. For example, the Bank of Japan, the Bank of Ghana, the Central Bank of Iceland, and so on.

The 12 Federal Reserve District Banks

The United States is broken up into 12 Federal Reserve districts. Exhibit 10-3 shows the boundaries of these districts. Each district has a Federal Reserve district bank. (Think of the Federal Reserve district banks as “branch

270 Chapter 10 Money, Banking, and the Federal Reserve System

E X H I B I T 10-3 Federal Reserve Districts and Federal Reserve Bank Locations

12

San Francisco

9 |

|

|

1 |

|

|

|

|

Minneapolis |

Cleveland |

2 |

|

|

Boston |

||

|

|

|

|

Chhicago |

7 |

|

New York |

|

|

||

10 |

4 |

3 |

Philadelphia |

Kansas City |

|

|

|

|

|

Board of Governors |

|

St. Louis |

|

|

|

|

|

(Washington, D.C.) |

|

8 |

|

5 |

|

|

Richmond |

||

|

6 |

|

|

Dallas |

|

|

|

Atlanta |

|

|

|

11 |

|

|

Alaska and

Hawaii are part

of the San Francisco

District

offices” of the Federal Reserve System.) Each of the 12 Federal Reserve district banks has a president. Which Fed district do you live in?

An Important Committee: The FOMC

The major policy-making group within the Fed is the Federal Open Market Committee (FOMC). A later part of this chapter will consider what the FOMC does, but for now you need only note that the FOMC is made up of 12 members. Seven of the 12 members are the members of the Board of Governors. The remaining five members come from the ranks of the presidents of the Federal Reserve district banks.

What Does the Fed Do?

The following is a brief description of six major responsibilities of the Fed.

1.Control the money supply. A full explanation of how the Fed controls the money supply comes later in the chapter.

2.Supply the economy with paper money (Federal Reserve notes). As stated in an earlier section, the pieces of paper money we use are Federal Reserve notes. Federal Reserve notes are printed at the Bureau of Engraving and Printing in Washington, D.C. The notes are issued to the 12 Federal Reserve district banks,

Federal Open Market Committee (FOMC)

The 12-member policymaking group within the Fed. This committee has the authority to conduct open market operations.

The Federal Reserve Board controls the nation’s money supply, but the Fed does not actually print money.

What government agency is responsible for printing our paper money?

271

You can read the bios of the members of the Board of Governors at www.emcp.net/

Board. The Fed operates an educational Web site at www.emcp.net/federalreserveeducation. Go there and click “American Currency Exhibit” to see some of the various currencies used in the United States at various times. You may want to click “In Plain English: Making Sense of the Federal Reserve.”

reserve account

A bank’s checking account with its Federal Reserve district bank.

which keep the money on hand to meet the demands of the banks and the public. For example, suppose it is the holiday season, and people are going to their banks and withdrawing greater than usual numbers of $1, $5, and $20 notes. Banks need to replenish their supplies of these notes, and they turn to their Federal Reserve district banks to do so.

Banks Becoming Partners

As the globalization trend continues, countries will open up

their banking sectors to the outside world. For example, on April 21,

2005, the Hangzhou City Commercial Bank, a local bank in Zhejiang Province, east China, and the Commonwealth Bank of Australia signed an agreement on strategic cooperation. The Australian bank purchased a 19.9 percent interest in the Chinese bank for 625 million yuan ($75 million). One of the reasons an Australian bank might want to be partners with a Chinese bank is because lending activities might be more advantageous (at some points in time) in China than in Australia.

ECONOMIC |

What might stimulate more of these types |

THINKING |

of bank partnerships in the future? |

The Federal Reserve district banks meet this cash need by supplying more paper money. (Remember, the 12 Federal Reserve district banks do not print the paper money; they only supply it.)

3.Hold bank reserves. Each commercial bank that is a member of the Federal Reserve System is required to keep a reserve account (think of it as a checking account) with its Federal Reserve district bank. For example, a bank located in Durham, North Carolina, would be located in the fifth Federal Reserve district, which means it deals with the Federal Reserve Bank of Richmond (Virginia). The local bank in Durham must have a reserve account, or checking account, with this reserve bank. Soon we will see what role a bank’s reserve account with the Fed plays in increasing and decreasing the money supply.

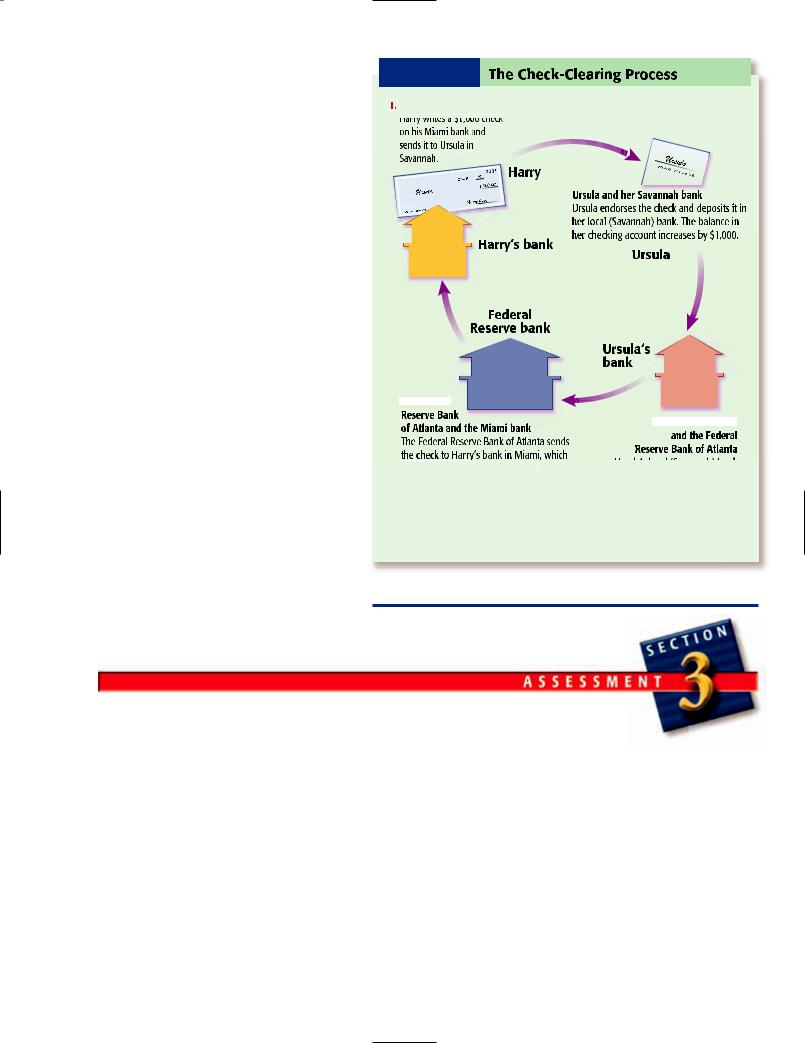

4.Provide check-clearing services. When someone in Miami (Florida) writes a check to a person in Savannah (Georgia), what happens to the check? The process by which funds change hands when checks are written is called the check-clearing process. The Fed plays a major role in this process.

Here is how it works (see Exhibit 10-4):

a.Suppose Harry writes a $1,000 check on his Miami bank and sends it by mail it to Ursula in Savannah. To record this transaction, Harry reduces the balance in his checking account by $1,000. In other words, if his balance was $2,500 before he wrote the check, it is $1,500 after he wrote the check.

b.Ursula receives the check in the mail. She takes the check to her local bank, endorses it (signs it on the back), and deposits it into her checking account. The balance in her account rises by $1,000.

c.Ursula’s Savannah bank sends the check to its Federal Reserve district bank, which is located in Atlanta. The Federal Reserve Bank of Atlanta increases the reserve account of the

272 Chapter 10 Money, Banking, and the Federal Reserve System

Savannah bank (Ursula’s bank) by |

E X H I B I T |

10-4 |

|

The Check-Clearing Process |

$1,000 and decreases the reserve |

|

|||

|

|

|

|

|

account of the Miami bank (Harry’s |

Harry and Ursula |

|

|

|

bank) by $1,000. |

|

|

||

|

|

|

|

|

d. The Federal Reserve Bank of Atlanta |

|

|

|

|

sends the check to Harry’s bank in |

|

|

|

|

Miami, which then reduces the bal- |

|

|

|

16-4 |

ance in Harry’s checking account by |

|

|

|

|

Miami, FL 91005 |

|

19 |

52 |

|

|

$ |

|||

|

Harry Jones |

|

|

|

|

1234 Anywhere |

|

|

2. |

$1,000. Harry’s bank in Miami either |

ay to |

|

|

|

Miami, FL |

|

|

|

|

|

P the order of |

|

|

|

|

a |

|

|

|

|

West Bank of Californi |

|

|

|

|

5678 Cashier Ave. |

|

|

|

keeps the check on record or sends it |

|

|

|

|

along to Harry with his monthly |

|

|

|

|

bank statement. |

|

|

|

|

5.Supervise member banks. Without warning, the Fed can examine the books of member commercial banks to see what kind of loans they made, whether they followed bank regulations, how accurate their records are, and so on. If the Fed finds that a bank has not followed established banking standards, it can pressure the bank to do so.

6.Serve as the lender of last resort. A traditional function of a central bank is to serve as the “lender of last resort” for banks suffering cash management problems. For example, let’s say that bank A lost millions of dollars and finds it difficult to borrow from other banks. At this point, the Fed may step in and act as lender of last resort to bank A. In other words, the Fed may lend bank A the funds it wants to borrow when no

4.

then reduces the balance in Harry s

s

account by $1,000.

3.

Ursula s local (Savannah) bank sends the check to the Federal Reserve Bank of Atlanta, which increases the reserve account of the Savannah bank by $1,000 and decreases the reserve account of

the Miami bank by $1,000.

An example showing how the check-clearing process works.

Defining Terms |

Reviewing Facts and |

||

1. Define: |

Concepts |

||

a. |

Federal Open Market |

2. |

In what year did the Fed |

|

Committee (FOMC) |

|

begin operating? |

b. |

Federal Reserve |

3. |

Explain how a check is |

|

System (the Fed) |

|

cleared. |

c. |

Board of Governors of |

4. |

What does it mean when |

|

the Federal Reserve |

|

we say the Fed is the |

|

System |

|

lender of last resort? |

d. |

reserve account |

Critical Thinking |

|

|

|

||

|

|

5. |

Economists speak about |

|

|

|

printing, issuing, and |

|

|

|

supplying paper money. |

Are these different functions? Where is each function performed?

Applying Economic

Concepts

6.Do you think banks need the Fed to act as “lender of last resort” more often during good economic times or bad economic times? Explain your answer.

Section 3 The Federal Reserve System 273