FinMarkets_BA14-2_03_mail

.pdfCoupon bonds

•Coupon Bond is a long-term contract under which a borrower agrees to make payments of interest and principal, on specific dates, to the holders of the bond

•A coupon bond pays the owner of the bond a fixed interest payment (coupon payment) every year (or more frequently) until the maturity date, when a specified final amount (face value or par value) is repaid

Moscow State University Business School

Financial Markets

Bonds

•For example, consider a 3 year bond with a face value of RUR 1000 and 12% annual coupons, paid semi-annually

–This bond has six coupons, each of which pays RUR 60

–After 3 years the company redeems the bond for RUR 1000

•Bond value is based on the present value of:

–A stream of coupon (interest) payments and

–The repayment of the par value at maturity

•How to calculate the bond market price?

–Bond price equals the present value of the bond’s cash flows

Moscow State University Business School

Financial Markets

Coupon bonds

•Consider a bond with a coupon rate of 10%, paid annually. The par value is RUR 1000 and the bond has 5 years to maturity. The yield to maturity is 10%. What is the value of the bond?

•Timeline

P PV |

C |

C |

|

C |

|

C |

|

N |

||

|

|

|

|

|

... |

|

|

|

|

|

1 i |

1 i 2 |

1 i 3 |

1 i n |

1 i n |

||||||

• Another point of view:

P PV PV of an annuity PV of the lump sum

Moscow State University Business School

Financial Markets

Quantitative problems (12)

•Consider a coupon bond that has a RUR 1,000 par value and a coupon rate of 10% (coupons are paid annually). The bond has 2 years to maturity and the yield to maturity is 8%. What is the bond’s current market price?

•Consider a coupon bond that has a RUR 1,000 par value and a coupon rate of 10% (coupons are paid annually). The bond is currently selling for RUR 1,150 and has 2 years to maturity. What is the bond’s yield to maturity?

Moscow State University Business School

Financial Markets

Quantitative problem (13)

• Consider a bond with a 7% annual coupon and a face value of RUR 1,000. Complete the following table:

Years to maturity |

Yield to maturity |

Current price |

3 |

5 |

|

3 |

7 |

|

3 |

9 |

|

6 |

7 |

|

9 |

7 |

|

9 |

9 |

|

• What relationships do you observe between maturity and YTM and the current price?

Moscow State University Business School

Financial Markets

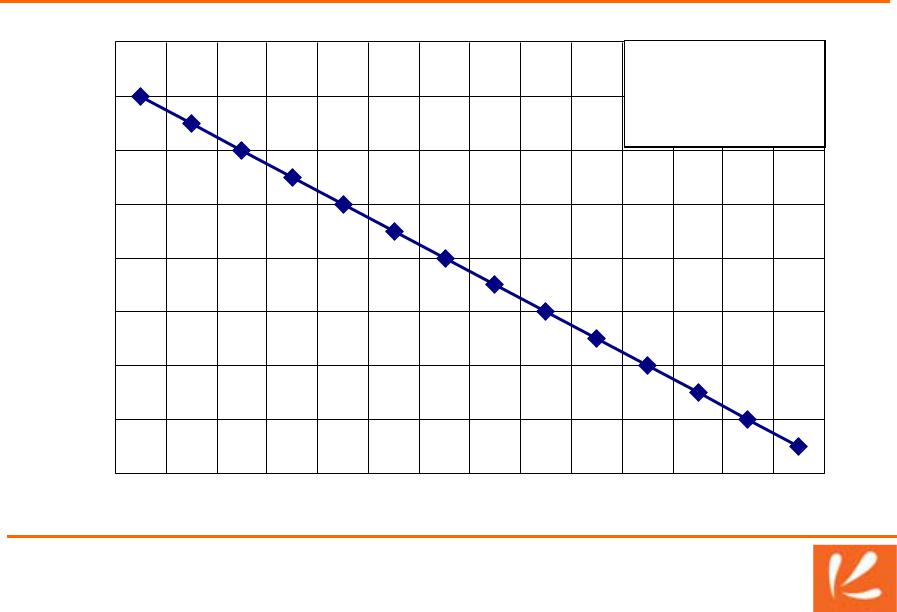

YTM and the price of a bond

16% |

|

|

|

|

|

Face = 1000 |

|

|

|

|

|

|

|

14% |

|

|

|

|

|

Coupon = 7% |

12% |

|

|

|

|

|

Maturity = 3 years |

|

|

|

|

|

|

|

10% |

|

|

|

|

|

|

8% |

|

|

|

|

|

|

6% |

|

|

|

|

|

|

4% |

|

|

|

|

|

|

2% |

|

|

|

|

|

|

0% |

|

|

|

|

|

|

837 |

858 |

880 |

902 |

925 |

949 |

974 1000 1027 1054 1083 1113 1144 1176 |

Moscow State University Business School

Financial Markets

Bonds

1 |

When yield to maturity is above the coupon rate, the bond’s |

current price is below its face value |

The opposite holds true when yield to maturity is below the coupon rate

2For a given maturity, the bond’s current price falls as yield to maturity rises

When yield to maturity equals the coupon rate, a bond’s

3current price equals its face value regardless of years to maturity

Moscow State University Business School

Financial Markets